Imagine a borrower submits a loan inquiry—and within 90 seconds, they receive a personalized text. They reply, answer a few quick questions, and by the time a loan officer sees the lead has come in, it’s already qualified. From cold inquiry to warm handoff, the entire sequence happens automatically.

When done right, that’s what texting for mortgage can look like.

There is plenty of data supporting the efficacy of SMS: texts have an average 98% open rate, compared to around 26% for email. No other channel comes close.

Yet despite those numbers, most mortgage teams still treat SMS as an afterthought rather than a growth lever. Today’s market doesn’t offer much runway for that gap to persist. High interest rates, tight inventory, and compressed margins mean fewer deals to go around.

Borrowers are simultaneously submitting inquiries to multiple lenders, and a 2026 survey of mortgage originators by National Mortgage News found that nearly two in three lenders admit they’re already losing business because they don’t have the loan officer capacity to follow up quickly and effectively.

This guide breaks down the data on why texting is effective for lenders, exactly how SMS for mortgage works, and how to use it to reduce funnel drop off—and stop losing leads you already paid for.

Why SMS is the number one channel for lenders

SMS outperforms other channels for mortgage outreach (and across other industries) by a wide margin. Here’s what the data says:

- 98% of text messages are read.

- 90% of SMS messages are read within three minutes of delivery.

- SMS has a 50% average reply rate (compared to just 1.4% for email).

- 78% of buyers would like to be able to message any business.

- 85% of U.S. adults use text messaging multiple times per week, across every generation and gender group.

- 37% of Americans say messaging has replaced most of the calls they used to make.

Verse covered texting in depth in our recent webinar, including how lenders are using AI-powered texting to respond faster and convert more of the leads they’re already paying for.

How does texting for mortgage work?

On the recipients’ end, business texting for mortgage teams works the same way personal texting does: a message goes to a borrower’s phone and they respond. The difference is what happens on the lender’s side.

Loan officers can text borrowers individually from personal devices, or they can use a business SMS platform. Rather than a loan officer typing messages one by one from a personal cell phone, business SMS solutions can manage outreach at scale, track conversation history, and connect with your CRM.

Messages can be triggered by lead activity, sent as part of a structured nurture sequence, or delivered as individual follow-ups—all from a centralized system your whole team can see.

Manual texting vs. SMS automation for lenders

Manual texting

Loan officers texting borrowers directly from their phones is already common practice. A personal text from a loan officer feels human, builds trust quickly, and can be highly effective during an active borrower relationship.

But manual texting has real limitations and risks that compound quickly:

No unified system. When LOs text from personal devices, there’s no shared conversation history. This can quickly become a problem because:

- If a loan officer is out sick, on vacation, or leaves the company, that entire thread of borrower communication is gone.

- Messaging cannot be standardized or tracked.

- There is limited or no visibility for management.

Compliance exposure. Individual loan officers texting from personal phones can inadvertently create TCPA violations: for example, missing opt-out language or texting outside of permitted hours. Without a managed system, compliance becomes dependent on individual awareness, which is not a reliable foundation.

High expectations. Borrowers who receive text messages from a business often expect fast replies at any hour—even when LOs aren’t working. For individual loan officers, this can become a burden and, at the same time, create customer dissatisfaction because expectations are not met.

Zero scalability. A single LO can only manage so many active threads. As lead volume increases, manual texting becomes a bottleneck.

SMS automation

SMS automation

Rather than relying on individual loan officers to initiate and manage every conversation, automation handles the high-volume, time-sensitive parts of the workflow.

SMS automation enables:

Instant 24/7 response. Automated SMS can respond to a new lead within seconds of form submission — regardless of whether it’s 9am or 2am. Over 40% of mortgage web leads arrive outside standard business hours, and most lending operations have zero live coverage during those windows. Automation closes that gap entirely.

Unified conversation history. Every message, reply, and interaction is logged in a central platform visible to the whole team. Managers can review conversations, spot patterns, and step in when needed.

Built-in compliance controls. A well-configured SMS automation platform enforces opt-in requirements, opt-out handling, permitted contact windows, and consistent messaging. This mitigates the compliance risks that come with unmanaged personal texting.

Scalability. Automation handles outreach across hundreds or thousands of leads simultaneously, without adding headcount. This way, LOs are only pulled in when a lead is qualified and ready for a real conversation.

How SMS reduces funnel drop-off

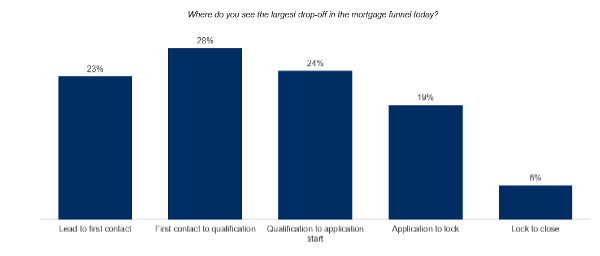

A February–March 2026 survey of mortgage originators conducted by National Mortgage News showed how borrower drop-off is distributed across every stage of the origination funnel.

When survey respondents were asked where they see the largest drop-off in the mortgage funnel today, the results were striking: 28% said first contact to qualification, 24% said qualification to application start, 23% said lead to first contact, 19% said application to lock, and 6% said lock to close.

That means the majority of drop-off is happening in the earliest stages: before a borrower has even started an application. Texting can be used to directly address and reduce drop-off at each stage.

Lead to first contact

This is where speed-to-lead determines whether a conversation happens at all. A borrower who submits a form and doesn’t hear back within minutes often moves on—or simply responds to whichever lender texted them first. In fact, research shows that 78% of people will choose the business that contacts them first.

Automated SMS eliminates the delay entirely, with responses going out within seconds of lead submission, 24/7. For example, Verse ensures every new inquiry receives a response within 90 seconds, regardless of when it arrives.

First contact to qualification

28% of mortgage pros said first contact to qualification was the largest source of borrower drop-off.

Borrowers may disengage for many reasons:

- Not enough follow-up

- LOs are reaching out on the wrong channels or at the wrong time

- Generic, non-personalized follow-ups

- Feeling rushed to apply too quickly

Two-way SMS changes the dynamic: it creates a low-friction, conversational environment where a borrower can answer a few qualifying questions on their own timeline, without committing to a phone call. We’ve already established that texting is the number one channel across age groups—and text messages can easily be personalized with lead data.

SMS automation can also follow up with leads that don’t reply, which can reduce drop-off at this stage for leads that aren’t sure if they’re interested, or forget to reply due to busy schedules.

Qualification to application start

Borrowers lose momentum when they don’t know what to do next, when they can’t easily get answers to basic questions, or when follow-up communication gets spotty after the initial exchange.

This is one of the highest-leverage places for automated SMS re-engagement. A borrower who started but didn’t finish an application is a warm lead, not a lost one. They just need a nudge.

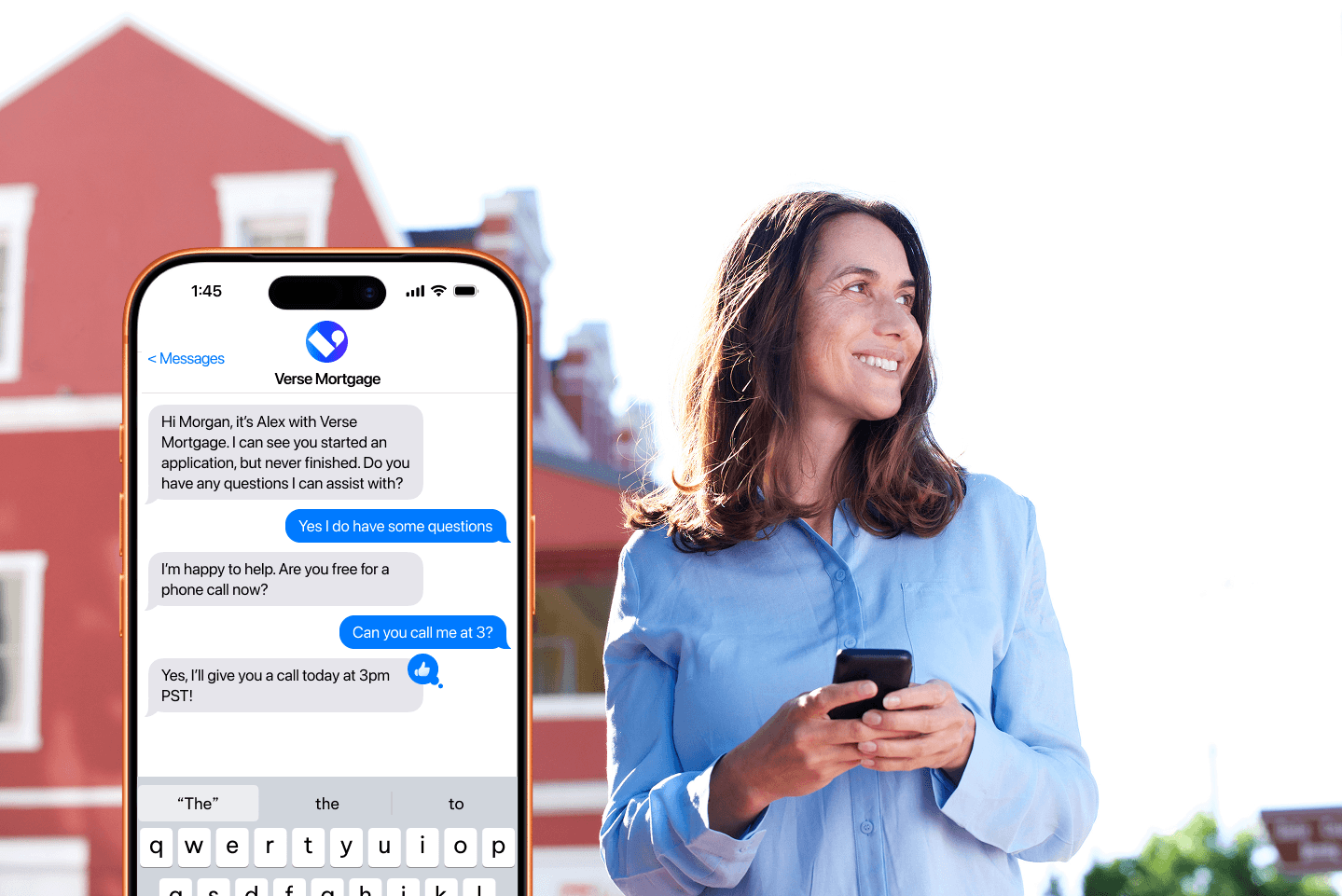

An automated text a day or two after qualification that reminds them about the application can be the difference between a completed file and a forgotten one. For example, sending a text like, “Hi [Name], it’s Alex with Verse Mortgage. I can see you started an application, but never finished. Do you have any questions that I can help you with?” not only reminds the prospect to finish, but shows that you’re invested and there to help.

Application to lock

Document requests and status updates are notoriously slow in the mortgage process. But these delays can cost you loans.

SMS reminders can propel the process forward throughout this stage. For example, a borrower who started an application but never finished is still a warm lead. Sending a text reminder reminding them to finish the application and checking if they have questions can be the difference between winning and losing the lead.

Borrowers who don’t hear from their lender assume something is wrong, start exploring alternatives, or simply disengage. SMS keeps the loop tight with automated updates at key milestones, quick document request reminders, and appointment confirmations.

Automated reminders that reference where they are in the process (“Hi [Name], Your file is at the underwriting stage. We’re waiting on your most recent pay stub to move forward”) help keep the borrower in the loop, boosting customer satisfaction. At the same time, this reduces loan officer effort and ensures that they don’t forget to send updates.

How mortgage lenders can leverage SMS automation

For mortgage teams, SMS automation solves a core operational tension: you need high-volume, consistent outreach, but adding headcount to achieve it drives up origination costs in an environment that’s already margin-compressed.

SMS automation handles initial outreach, follow-up, and nurture without requiring loan officer involvement, freeing your team to focus on conversations with borrowers who are actively engaged. When a borrower is qualified and ready to move forward, they’re routed to a loan officer with full conversation context already in hand.

SMS platforms like Verse also integrate directly with your CRM. Every text sent, every reply received, and every qualification data point gets logged in real time, so pipeline visibility is maintained, follow-up cadences are enforced automatically, and no lead falls through a gap between your texting system and your loan management workflow.

AI texting for mortgage lenders

What about AI?

AI texting can be a part of SMS automation that improves conversation quality. Of course, it’s critical to choose and manage customer-facing AI carefully.

While basic SMS automation sends pre-written messages on a schedule, AI texting reads and responds to what a borrower actually says, handling follow-up questions, adjusting tone based on context, and continuing a conversation naturally.

For example, borrowers asking about rate locks, pre-qualification requirements, or loan types need relevant, accurate responses. AI can be trained on your datasets in order to handle these questions.

When AI is trained and controlled properly, it can handle those conversations in a meaningful, compliant way: it operates within guardrails set by your team, ensures every message meets regulatory requirements, and escalates to a human agent at the right moment.

The result is a borrower experience that feels personal and responsive, and an operational workflow where loan officers only engage when and where they add the most value.

How Verse texting supports mortgage companies

Verse is an AI-powered, fully managed conversational platform built for mortgage teams that want to use AI texting without any of the risk or manual work involved.

With an established track record managing millions of mortgage leads annually, Verse is a trusted partner for some of the industry’s most respected brokers and lenders. Verse helped Acra Lending boost response rates by 133% with 24/7 coverage via SMS with instant replies.

Verse supports mortgage teams with:

- 24/7 instant lead response via text

- Custom qualification scripts

- CRM integration

- Compliance built in

When every lead matters and loan officer capacity is a genuine constraint, Verse turns texting from a manual burden into a scalable, high-converting system.

Learn more by booking a demo or exploring our self-serve demos here.

Key takeaways